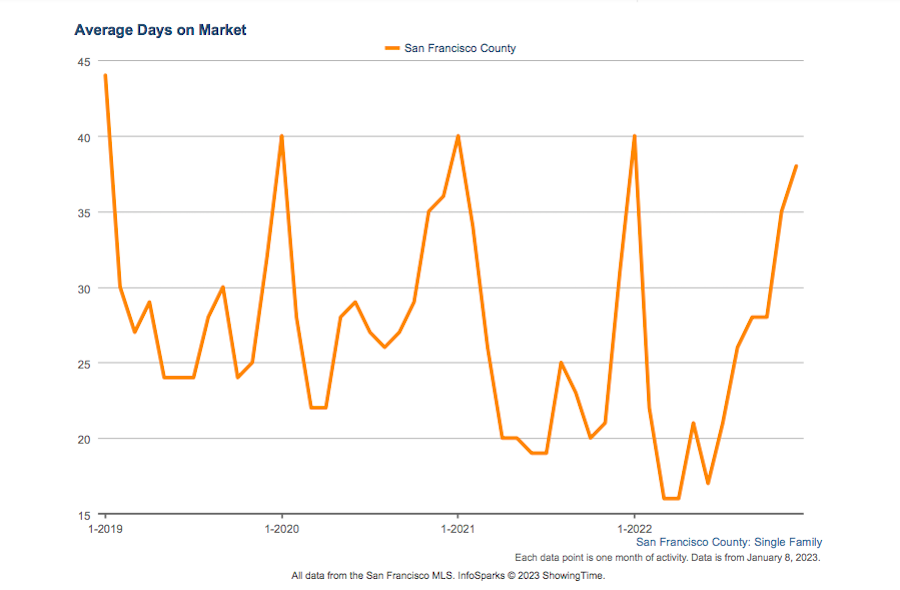

A testament to the market slowdown amidst elevated mortgage interest rates, recession jitters and geopolitical unease, only 1,113 Single-Family and Condo/TIC/Coop properties sold in Q4 2022. This is the lowest number for the quarter since 2008, and a dramatic decrease of 40+ percent from just one year ago (which at 1,953 is the highest in almost two decades).

What Does 2023 Have On Tap?

There is a plethora of conflicting predictions about where home prices are headed. Locally, home prices are unlikely to budge by any significant measure. Higher interest rates, stock market volatility and job market anxiety will affect what buyers are able and willing to pay. And sellers who don’t have to sell will stay put instead of negotiating and accepting a less-than-desirable price. All in all, expect a more balanced market, stable prices, and much less sales activity.

With limited inventory to choose from, competition among buyers may heat up for the best properties. Bargain hunters will be disappointed, and well-qualified buyers will prevail. Assuming the hybrid work model is here to stay, those homes that accommodate an office area and have a functional separation of space will lead the pack. A recession could put downward pressure on both property values and mortgage interest rates, creating a window of opportunity — but also unleashing demand that overwhelms supply.

So-called strategic underpricing will continue to be a risky move in 2023 because buyers are not in the mood to overbid. Thus, more sellers will list at or above market value, and most likely spend more time on the market before going under contract. Perhaps strategic price reductions, creating the perception of a good deal, will be sellers’ key to hitting their magic number. That said, there will always be that snazzy house in a prime neighborhood which lists for 30+ percent under value and drives a massive bidding war.

Don’t expect benchmark 30-year fixed mortgage interest rates to drop toward the all-time lows of late 2020, or even into the 4 percent range. Easing inflation and economic contraction could well lead the Fed to reverse course on rate hikes, however our trusted lending partners unanimously predict that rates at or above 5 percent are here to stay. The borrowers best positioned for success will be those who remain mindful of the longterm historical averages, follow guidance to “marry the house and date the rate,” and aggressively negotiate deals while it’s still possible.