Home Buyer Tips: Navigating High Prices & Borrowing Costs

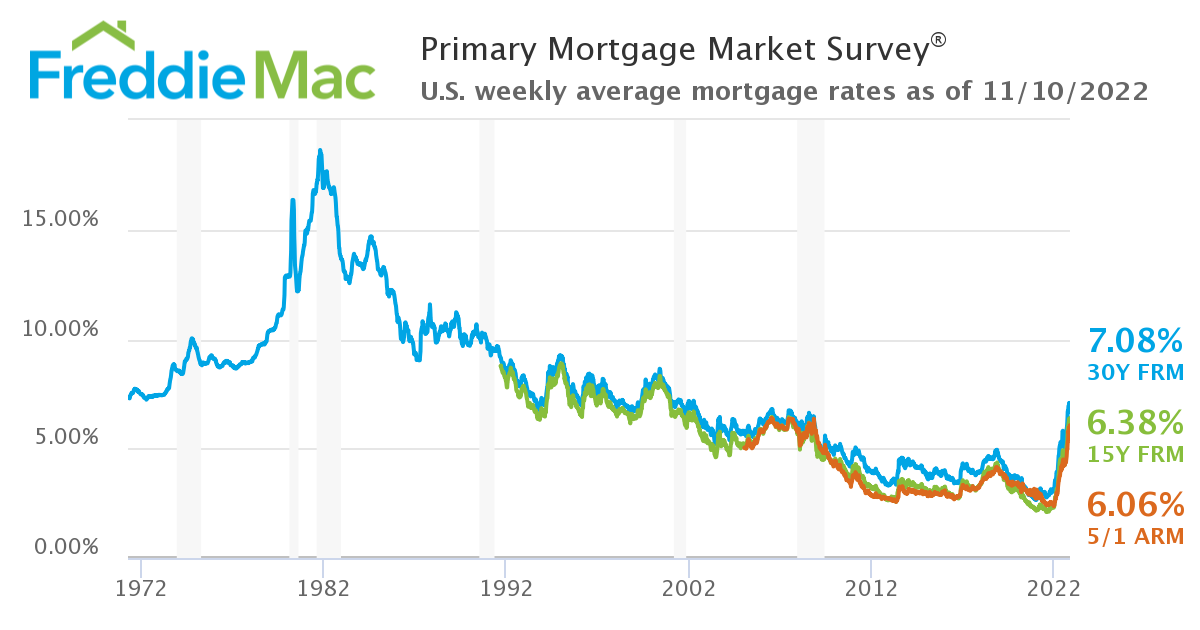

Having begun the year at 3.22 percent, Freddie Mac’s benchmark 30-year fixed interest rate has more than doubled — and the anguish of home buyers is palpable. Those who attempted to time their purchase (and are still waiting) for the deal of a lifetime now face the prospect of a monthly mortgage payment higher by thousands of dollars, all else equal. Unfortunately, median sales prices for both Single-Family and Condo/TIC/Coop properties are also up from January and almost certainly headed higher thru at least the first half of 2023.

Freddie Mac’s Primary Mortgage Market Survey results from its inception in 1971 to present. The benchmark 30-year fixed rate reached an all-time high of 18.63 percent in October 1981. Source: freddiemac.com

This is not uncharted territory, however. While the benchmark 30-year interest rate was largely above 6 percent from 1996 thru 2007, San Francisco’s median sales price rose each of those years according to SFAR MLS data. Rates actually peaked above 8 percent multiple times during that period. And Since 2012, the city’s median sales price has again increased each year and is on track to eke out a new record in 2022.

At first glance, the confluence of today’s high home prices and borrowing costs — alongside layoffs just announced by a handful of the Bay Area’s largest employers — may appear to signal that a crash a la 2008 is nigh. Be not afraid! Simply put, the factors that precipitated the 2008-2011 housing bubble burst (i.e. predatory lending, unregulated markets, abundance of inventory, etc.) are essentially non-existent today.

Median sales price numbers reported to SFAR MLS as of 15 November 2022 for residential properties. Each data point represents 12 months of activity. Information is deemed reliable but not guaranteed and is subject to change.

Whatever economic turbulence the real estate market may experience, it is unlikely that we’ll see a Great Recession 2.0 where the median price falls over a prolonged period of time by 20+ percent. Consensus among industry insiders is that 2023 will see fewer buyers, fewer sellers, and overall a decrease in sales activity from recent years — perhaps 30 percent lower than in 2021 according to Redfin CEO Glenn Kelman.

It is possible that San Francisco is already on the cusp of the next upswing. The latest data from SFAR MLS shows sales activity down approximately 30 percent for the year — and accompanied by prices moderating, not declining. For what it’s worth, the city is historically faster in its recovery than other parts of the country. It is, after all, a fundamentally robust market, one of the most desirable in the world, with a perennial undersupply of housing and new construction severely limited by geographic and political constraints.

Number of sold Single-Family and Condo/TIC/Coop properties reported to SFAR MLS as of 15 November 2022. Information is deemed reliable but not guaranteed and is subject to change.

With only six weeks left in the year, San Francisco’s Condo/TIC/Coop segment has seen an almost 40 percent drop in number of closed sales year-to-date compared to all of 2021. Median sales price is relatively unchanged ($1,210,000 in 2021 vs $1,200,000 in 2022 YTD) and so, too, is the average number of days a listing is on the market before sale (42 days in 2021 vs 39 days in 2022 YTD).

The number of Single-Family home sales is down approximately 30 percent year-to-date compared to all of 2021. The median sales price is unchanged at $1,800,000 but the average number of days a listing is on the market before sale increased from 12 to 21 days. For all property types, the number of listings given price reductions and withdrawn from the market is up significantly.

In light of all this, here are a four money saving tips for home buyers:

› Explore both conforming and jumbo mortgage products. Interest rates for conforming loans (up to $970,800 in San Francisco) are currently between 0.5 and 1 percentage point higher than jumbo rates due to fees and restrictions imposed on Fannie Mae and Freddie Mac. Instead of making a 20 percent down payment and obtaining a conforming loan, borrowers may lower their monthly payment and keep more cash on hand by putting 15 percent down, for example, and going with a slightly larger loan amount.

› Negotiate credits from the seller to lower effective purchase price. In the absence of budging on price, many sellers are willing to give money back to buyers in escrow. Such a credit may be applied toward closing costs, an interest rate buy-down (see below), or any number of expenses on a case-by-case basis. Taking a cash credit now and refinancing to a lower interest rate in the future is one way buyers can enjoy both immediate and longterm savings. Most lenders limit the amount of money a seller can credit the buyer. This is typically 3 to 6 percent of the purchase price, or not to exceed the total amount of the buyer’s closing costs.

› Consider adjustable-rate and interest-only mortgages. Loans where the interest rate adjusts after 3, 5, 7 or 10 years typically have lower starting rates than longer term fixed-rate products. This is especially advantageous for borrowers who plan to sell within a few years; if plans change, refinancing to a 30-year fixed mortgage is always an option for the risk averse. For those wanting a 30-year fixed mortgage from the get-go, it could still make sense to lock in a low adjustable-rate now and refinance next year assuming rates drop below current levels once inflation is tamed.

› Pay points to lower your interest rate. One point is 1 percent of the borrower’s loan amount. Paying a point could lower your rate .25 to .5 percent depending on the lender and market conditions. A lower interest rate in turn decreases the monthly payment which may add up to thousands of dollars in savings over several years. It is important for a borrower to get their lender’s approval for a buy-down credit upfront; this is not an arrangement that the buyer and seller can structure without lender participation and approval.

You can always live chat with us to get real-time data and a qualitative take on the market. We’re actively identifying unique opportunities and making deals happen. We know what’s good!

Subscribe to broker insights, top headlines, off-market listings, and new development launches delivered monthly to your inbox.

SF House & Condo/TIC/Coop Market Metrics, April 2024

The following is adapted from the April 2024 Monthly Indicators report published by the San Francisco Association of REALTORS®. Elevated mortgage interest rates and rising...

SF Askhole Of The Month, April 2024

If the head-turning world of San Francisco real estate has any constant no matter the times, it's OUTRAGEOUS overbids. Indeed, local agents have a unique and longstanding...

2177 Third Is 80% Sold, New Home Prices Reduced

When it comes to modern condominium developments in the Dogpatch neighborhood, 2177 Third is the standout. Premium is the standard here, from resident concierge and valet...

What $1 Million Buys In SF’s North Panhandle

As the Median Sales Price in San Francisco continues to rise — up ±18% from the start of the year — homes priced to sell under $1 million are increasingly hard to find. In...

Inside The $13 Million Penthouse At 181 Fremont

Word on the street is that San Francisco's condo market is on the mend. According to data reported to the San Francisco Association of REALTORS®, last month's Median Sales...

Home On Alamo Square’s “Seattle Block” Prepares For Sale

The world-famous painted ladies of Postcard Row draw millions of visitors to Alamo Square each year, but the historic district has no shortage of eyepopping real estate all...

SF House & Condo/TIC/Coop Market Metrics, March 2024

The following is adapted from the March 2024 Monthly Indicators report published by the San Francisco Association of REALTORS®. Across the country, existing-home sales...

VIP Homes For Sale: Janis Joplin, Haig Patigian, Ken Fulk

It's a line as true today as it was when Paul Kantner said it over a half-century ago: San Francisco is 49 square miles surrounded by reality. Indeed, it's an undeniably...